Where we are with impact investing: a conversation with Adam Robbins, Triodos IM

Every investment has an impact, says Adam Robbins, Head of Business Development at Triodos Investment Management. “Some are positive, others aren’t.”

Impact investing was formulated on the thesis that every investment should have a positive influence, whether on environment or society. The sector boasts more than $1tn in assets as of 2022, according to the Global Impact Investing Network (GIIN), yet its continued branding as a separate asset class is what frustrates proponents of its all-encompassing avatar.

As for the Sustainable Development Goals (SDGs) – the global objectives that form guardrails of the impact space – the world remains well off-target. Speaking on a webinar organised by Oxford’s Said Business School last year, Amie Patel, a Partner at Elevar Equity with over 20 years of experience investing in emerging markets, argued that more than $4tn per year was required to deal with issues –including poverty – that affect the global majority.

A shift in perception away from impact being a class of investments, towards a baseline for all deployment, is key to unlocking those levels of capital. Robbins says: “We’re not there yet, but I do think there is evidence of change. There is more interest from larger institutional investors, for one. And real-life events – such as the unprecedented frequency of named storms we’ve had in the UK this year, or the flooding in Dubai, to name a few – are all fuelling momentum in this space.”

The duality of performance

Robbins points out two central blockers to progress. One is a perennial issue, namely the scepticism that surrounds the space about the real influence these investments can have. The second, a more cyclical problem, is a flight towards what are perceived to be more financially stable or lucrative investments at a time of uncertainty.

As expected, the latter tendency has manifested amid recent economic turbulence. “Whether on the public markets, where consumers are feeling the cost-of-living squeeze, or the private markets, financial return has been more important for investors than positive impact.

“It’s been hard going for impact investing in the last two quarters, particularly when comparing against traditional benchmarks such as utilities, oil and gas, financial services and so on. Strong performance in the passive market has been a factor – allowing investors to trim off excess costs. It’s hard for impact investing to compete there as you can’t have a genuine impact solution that’s passive or index-based.

“In general, negative messaging in the press around the renewables and sustainability sector has not helped matters.”

There are important caveats when discussing financial performance. Compared to other alternatives, Robbins says the impact world is starting to make a comeback this quarter. “Most institutional investors have their own measurement frameworks – commonly to benchmark against the MSCI ACWI. A number of impact funds out there are currently performing very much in line with that index, if not above it,” says Robbins.

That said, impact investing was never meant to be purely evaluated from a financial standpoint. But the fact that the task of measuring real positive impact remains shrouded in ambiguity is the root cause of the other main blocker to progress in this space – scepticism.

Impact investing is traditionally measured along environmental, social and governance (ESG) metrics, and there is notable nuance in how performance can be measured in each area.

Robbins says: “Environmental factors are clearly the simplest to measure. Many fund launches in the impact space are targeted at the climate energy transition, aligned with Paris agreement objectives. And the fact that large institutional investors are under pressure to decarbonise their portfolios and reduce greenhouse gas (GHG) emissions sets a clear scope for progress there.

“The social side of it is far more tricky, as it’s less tangible, and measuring via taxonomy and other benchmarks can be ambiguous. As for governance, it should be an implicit hygiene factor for most companies, portfolios without good governance wouldn’t get listed on the public side, or even considered in private markets.”

Reconciling both factors – the prospect of financial return with real positive change – remains the defining challenge of impact investing.

Robbins share a success story from within Triodos – their microfinance fund that represents the financial inclusion pillar of impact. Over a track record of 25 years, he reports the fund has had only had one year of negative return due to Covid, clocking north of 4% per annum in returns all other years. That’s in addition to having a tangible positive impact.

Windows of opportunity

There are green shoots of recovery across the private markets landscape this year – conditions may still be challenging, but there is a degree more of certainty on the future. This is filtering through to the impact space, Robbins says.

“The US has really started to up its game in terms of impact and sustainability. There’s also good upside to be had on European investments at this point in time, while Japan is a very interesting market too as it’s massively undervalued. We’re primarily focused on private markets, and we’re seeing an uptick in activity in emerging markets in particular,” he says.

As for unlocking capital to raise the profile of impact investing, Robbins suggests there is plenty of opportunity for financing. “If we take the example of Australian superannuation funds, for instance, there are billions in that market seeking impact investing opportunities, but they simply don’t have enough fund managers there to service the demand. And there are other similar cases, where significant chunks of capital can be moved around to inject more momentum and affect real change.”

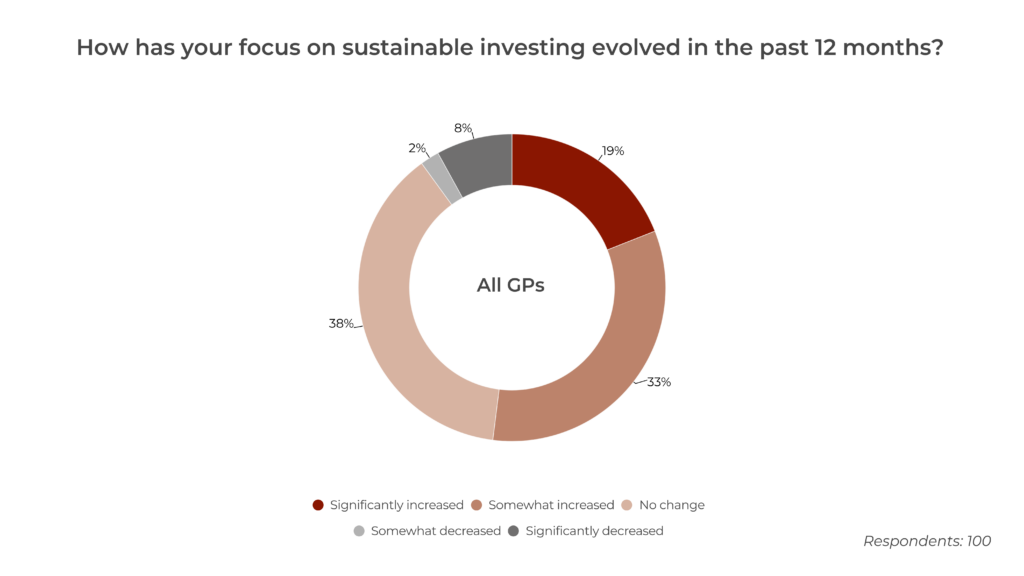

Private Equity Wire’s Q1 GP survey revealed more than half (52%) of all managers have increased their focus on sustainable investing in the past 12 months – a truly positive indicator for the road ahead.