Two opposing forces are apparent in private markets this week – the withdrawal of wealth and retail capital from private credit funds, and steps towards the invitation of retirement pools into private capital as a whole. Here’s analysis from Private Equity Wire’s® Editor, Aftab Bose.

The successful conflation of these forces is predicated on education and discipline.

Yes, there has been a spike in redemptions from non-traded BDCs, but these make up a small sliver of total private credit AUM.

Yes, there has been an increase in gating, but this is a minor fraction of total redemptions, is built into fund terms and is, in large part, imposed for the protection of long-term returns.

Yes, there have been defaults, but these will continue to come as a result of irresponsible gold-rush lending in segments of the market, and usually won’t relate to the brand name players.

And yes, there is exposure to software, but lending is, for the large part, less susceptible to valuation fluctuations than your average stock investment.

This is not to say that private markets investments don’t entail risk, and that the market isn’t susceptible to spurious valuations and subsequent liquidity shocks. We’ve seen this in a very material manner in recent years. But the above nuance will have to be bedded into the retail psychology in the long run if the 401k experiment is to truly be successful.

We can expect a steady stream of headlines in months to come, as a range of highly scrutinised practices – such as cov-lite lending, amends-to-extend, payment-in-kind and others – arrive at their final point of maturity, revealing the most realistic picture yet of default rates.

The resultant redemption and gating cycles in semi-liquid funds will force managers with these offerings to reckon with their valuation mechanisms, liquidity practices and, perhaps most importantly, their ability to communicate with and educate end investors. All of the above were cited among the biggest challenges currently being faced in private credit.

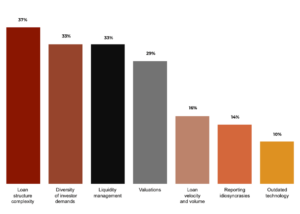

Biggest operational challenges in private credit

Firms are caught in a paradoxical doom loop of sorts. Retail investors are demanding a higher frequency of valuations, which in itself is an operationally intensive exercise – with limited credibility given the opacity of data and valuation mechanics in private markets.

One area that is falling into favour is asset-based financing, which has a number of inherent structural protection mechanisms.

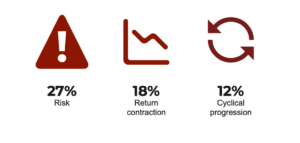

Top reasons to diversify away from direct lending

For one, covenant practices are going in opposite directions, with direct lending famously moving towards cov-lite terms while ABF remains covenant-heavy. Another difference is in the reliance on company valuations. Jennifer Marques, Managing Director and Head of Strategy and Structuring at Oaktree explains: “In ABF, investments are self-amortising. As the underlying borrowers pay interest, they’re also paying off principal so the investment is being amortised down.

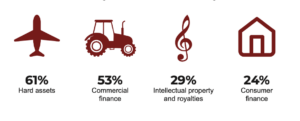

Top areas of interest in asset-based financing

“To pay down the principal in direct lending, in contrast, there needs to be alignment in the valuation of the asset. ABF doesn’t require a valuation exercise, it just requires the underlying loans in the SPV to repay. Our investments also tend to be shorter duration – two-to-four years compared with five-to-seven years in direct lending. That’s a fundamentally different risk profile.”

Read all about this and more in our latest private credit report.