Using Preqin’s new fund size benchmarks on Hedge Fund Analyst, together with the results of our interviews with approximately 300 hedge fund managers, this extract from September’s Preqin Hedge Fund Spotlight newsletter analyses the effect that fund size has on the overall hedge fund industry by looking at performance, terms and conditions, and the fund sizes institutional investors are looking for.

In July, Preqin added a new series of benchmarks to our Hedge Fund Analyst online service. These benchmarks, which assess the performance of hedge funds based on the size of the fund, can be used in tandem with our strategy, regional, structural and currency benchmarks. Following the launch of these benchmarks, Preqin has turned its attention to the effect of size on the industry, as we take a look at what size funds institutional investors look for, provide a breakdown of the industry by size and look at how the performance of hedge funds varies by fund size. The results found in this study are based on Preqin’s award-winning Hedge Fund Online service and June interviews with approximately 300 hedge fund managers.

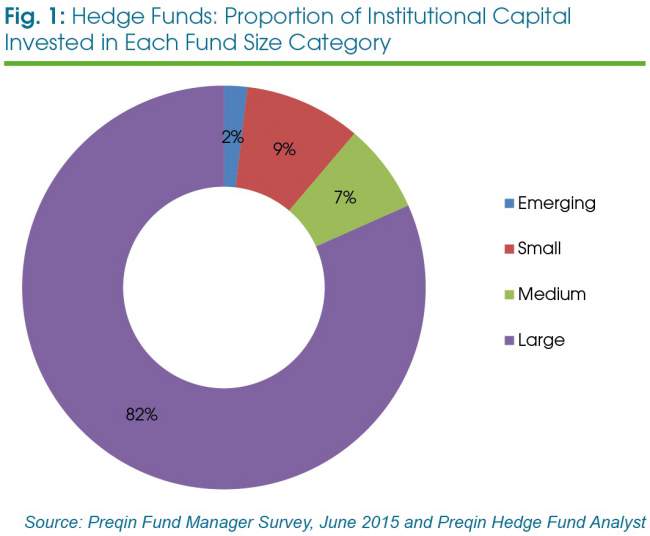

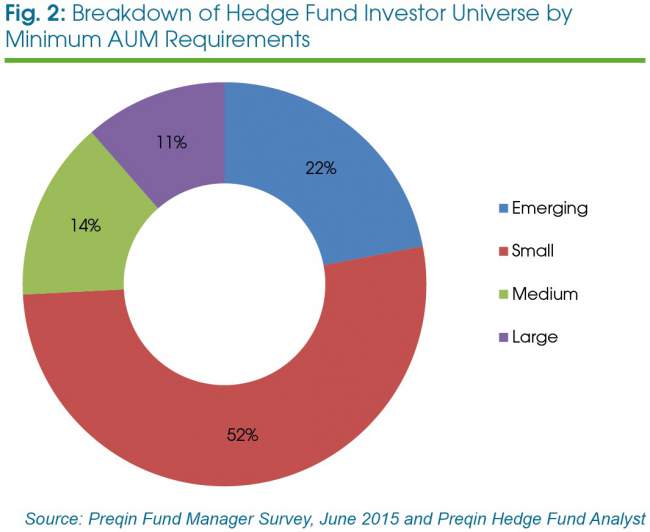

Preqin’s Hedge Fund Manager Outlook recently revealed that 66 per cent of capital in the industry today is sourced from institutional investors. As shown in Fig 1, over four-fifths of institutional capital is invested in hedge funds which have at least USD1 billion in assets under management (AUM). Although the large majority of institutional capital is concentrated in the largest funds, investors retain an appetite for smaller funds. Fig 2 shows the breakdown of investors by their minimum AUM requirements of hedge funds before they will consider investing in them. Just 11 per cent of investors will consider investing exclusively in funds with more than USD1 billion in AUM. Although a relatively small proportion (22 per cent) will consider investing in funds with less than USD100 million in AUM, over half (52 per cent) have a minimum requirement that lies between USD101 million and USD499 million.

Looking at the minimum AUM requirements by investor type, again, excluding funds of hedge funds, it is private wealth organisations or those institutions that have larger or more sophisticated hedge fund portfolios that are most likely to invest in smaller funds. Fifty percent of wealth managers and 38 per cent of both endowments and family offices will consider investment in the smallest funds (those with less than USD100 million in AUM). In contrast, only 6 per cent and 7 per cent of private sector pension funds and foundations respectively will consider emerging funds, in terms of minimum AUM.

These results suggest that even though institutional investors are putting large amounts of capital to work in the biggest funds in the industry, a smaller investment in smaller funds is still a common option for many investors.

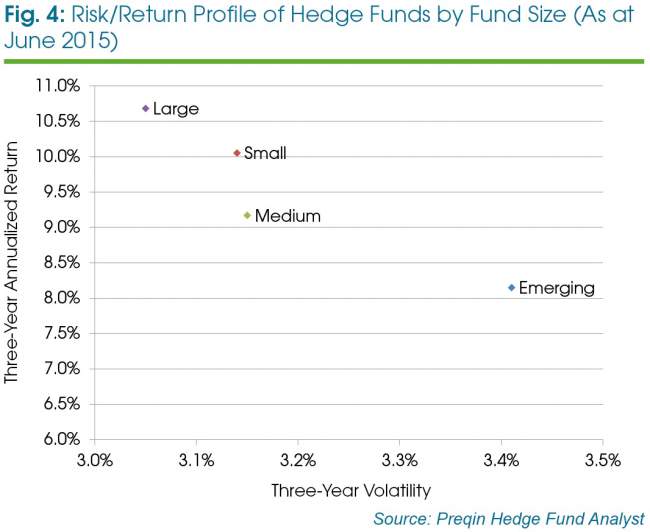

Large funds have the most attractive risk/return profile

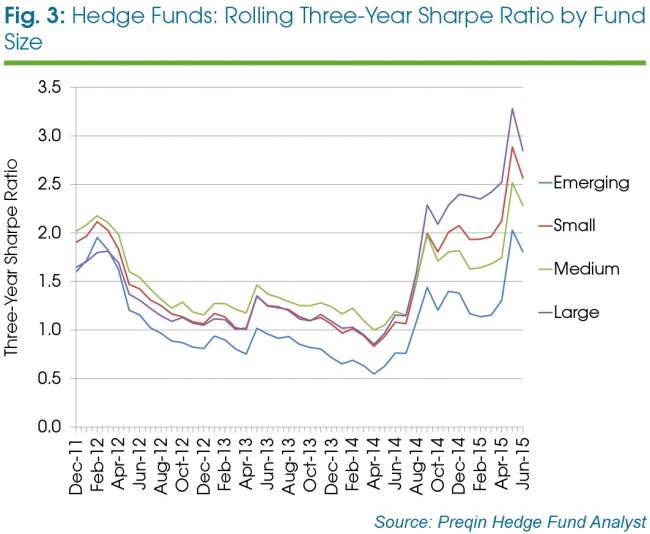

With over 80 per cent of all institutional capital invested in funds with more than USD1 billion in AUM, it is important to assess how these funds are faring in terms of performance. When looking at returns on a risk-adjusted basis, funds with more than USD1 billion in AUM have produced the highest three-year annualised returns (as of 30 June 2015) with the lowest volatility (Fig 5). Funds with less than USD100 million in AUM, in contrast, have produced the lowest three-year annualised returns (as of 30 June 2015) with the highest level of volatility. The rolling three-year Sharpe ratio of all hedge funds, regardless of size, has been increasing since mid-2014 (Fig 3). As of June 2015, large funds, those with more than USD1 billion in assets, have the highest three-year Sharpe ratio (2.84), its highest over the period examined. In fact, large funds have shown the best performance over the past 12 months (to June 2015), which has led to their rolling three-year Sharpe ratio to overtake that of small and medium sized funds.

When looking at funds in the range of USD100-999 million, it is those in the first part of this group that exhibit the more attractive risk-adjusted returns. Funds of USD100-499 million exhibit higher three-year annualised returns (+10.05 per cent to 30 June 2015) with a comparable level of volatility to funds in the range USD500-999 million.

Large funds have built up assets over many years; the average track record of a fund with assets of USD1 billion or more is 12 years. These funds were able to distinguish themselves from their peers when they were smaller, in terms of better returns, which investors rewarded with capital commitments. Therefore, in the larger fund groups there has been selection for the better performing funds on an absolute and risk-adjusted basis, a reason why this group as a whole performs better than their smaller counterparts.

Smaller funds can offer more favourable terms and conditions

If the largest funds are currently offering better risk-adjusted returns than funds with less than USD1 billion in AUM, why are investors continuing to consider investment in smaller funds? The distribution of 12-month returns of large funds is more concentrated, with 50 per cent of funds exhibiting returns between 1.88 per cent and 11.74 per cent over the 12-month period to June 2015. In contrast, small funds show a greater dispersion of returns with both greater minima and maxima. Therefore, in the smaller categories there will be a large number of new funds, some of which will underperform and potentially liquidate as they fail to meet expected return requirements. Although some smaller funds will underperform, there are also funds distinguishing themselves through better performance compared to funds of all sizes.

Owing to their strong risk-adjusted returns, longer track records and greater investor appetite for larger funds, these vehicles can demand higher management and performance fees. In addition, a larger proportion of these funds are closed to new investment as they are at full capacity. Smaller funds, those with less than USD500 million in assets, also typically charge lower fees and a greater proportion are open to investment. Therefore when investing in smaller funds, investors will be trying to pinpoint those funds that are outperforming their peers and also invest in funds that may have lower fees than their larger counterparts. As an early investor in a fund, an institution may retain these favourable terms and conditions if the fund grows due to its success.

Outlook

The hedge fund industry has continued to grow over the first half of 2015. Today Preqin estimates that industry assets have surpassed USD3.1 trillion and institutional capital accounts for almost two-thirds of this sum. The bulk of this institutional capital is invested in the largest funds (more than USD1 billion in AUM). In total, this group represents 9 per cent of all funds in the hedge fund industry today; therefore a large amount of capital is invested in a relatively concentrated group of funds. Currently this capital is well invested: as of 30 June 2015, funds with more than USD1 billion in assets have the highest three-year returns and the lowest volatility. However, investors retain an interest in smaller funds, with nearly three-quarters of institutional investors stating a minimum AUM requirement of less than USD500 million.

This article is drawn from Preqin Hedge Fund Spotlight | September 2015. Read the full newsletter for free here.