The average time taken to exit private equity-backed buyout investments has increased year-on-year since 2008. In this extract from the Preqin Private Equity Spotlight: May 2015, Anna Strumillo and Ciantelle Lawrence conduct an in-depth analysis of buyout holding periods.

Private equity investments are traditionally long-term investments with typical holding periods ranging between three and five years. Within this defined time period, the fund manager focuses on increasing the value of the portfolio company in order to sell it at a profit and distribute the proceeds to investors. This in turn determines how quickly and how much the investors can recycle back into the asset class through new fund commitments. Therefore, the holding period of portfolio companies can have a significant effect on private equity firms’ ability to raise future funds as well as on the whole private equity cycle in general.

Data from Preqin’s Buyout Deals Analyst shows that the average holding period has increased substantially in recent years. The shift is unsurprising given the tough economic conditions faced in the post-crisis era, leading to buyout fund managers finding it increasingly difficult to make a profitable exit from their investments.

However, despite this overarching longer term trend, the exit environment appears to be fervent with the number and total value of private equity-backed exits in 2014 reaching their highest levels on record. In fact, Preqin’s latest 2015 YTD exit data shows a reduction in the average holding period which may indicate a significant milepost has been reached.

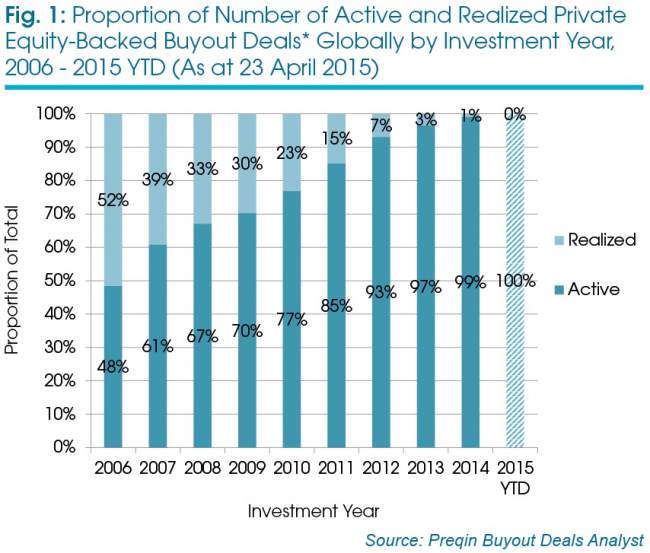

Deals yet to be exited

Based on the traditional practice of private equity firms holding their investments for three to five years, it was expected that the majority of portfolio companies purchased during the buyout boom of 2006-2007 would have been exited by now. However, as Fig 1 shows, 48% of companies acquired in 2006 are yet to be fully realised, while the corresponding proportion for those investments made in 2007 currently stands at 61%. This is in comparison to 57% and 67%, respectively, a year ago.

Average holding period

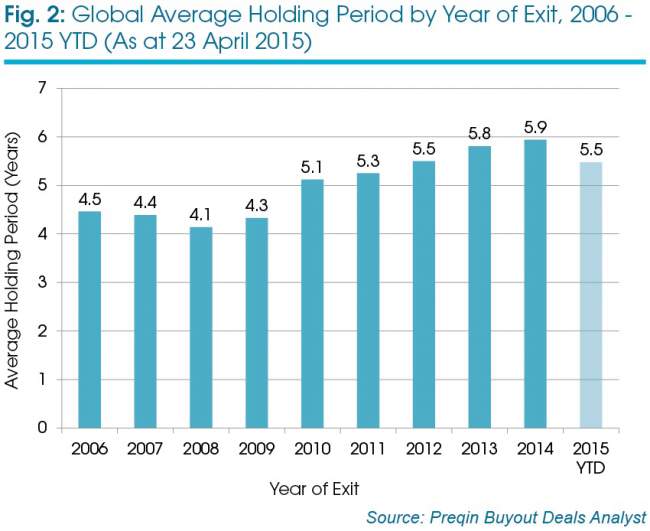

As illustrated in Fig 2, the average holding period for portfolio companies for private equity buyout fund managers has increased significantly over recent years, from 4.1 years in 2008 to 5.9 years in 2014. This increase further alludes to the difficulties found in exiting companies acquired at high valuations during the buyout boom. While not a full year figure, Preqin’s latest data shows that the average holding period for portfolio companies exited in 2015 YTD has dropped to 5.5 years. This goes to underline the favourable exit conditions which on the one hand have created a sellers’ market, and on the other, an opportunity for buyout managers to deploy some of the estimated USD469 billion in dry powder at their disposal via secondary buyouts.

While just over half (53%) of portfolio companies fully exited in 2006 had been held by private equity firms for under four years, this proportion dropped to 26% of all companies exited in 2012 and currently stands at 32%. The opposite trend can be observed for companies held by private equity firms for seven to nine years: in 2006, the portfolio companies fully exited after being held for this period accounted for 12% of all companies exited that year; this proportion increased to 29% in 2014 and stands at a quarter of all companies exited in 2015 YTD.

Nonetheless, there are some notable investments which are exceptions in the trend of longer holding periods, such as Warburg Pincus’ investment in JHP Group Holdings, Inc. Warburg Pincus held the company for just over a year and in early 2014 sold it to TPG-backed Par Pharmaceutical Companies, Inc., reportedly reaping three-times their investment. Similarly, earlier this year, Clearlake Capital Group made a quick three-times return on their investment in PrimeSport, Inc. after holding a stake in the company for less than 12 months.

Geographic variations

There are notable geographical variations in average holding periods for private equity-backed deals. Since 2006, the average holding period for portfolio companies based in North America increased from 4.4 years in 2006 to a high of 6.0 years in 2014. Europe, however, has the longest average holding period of all regions at 6.2 years for deals exited in 2014, compared to a European low of 4.1 years in 2008. The holding period for Asia-based portfolio companies has increased from 3.4 years in 2007 to 5.6 years for companies exited so far in 2015, while holding periods in the Rest of World region increased from a low of 3.1 years in 2008 to a high of 5.5 years in 2012 and 2013.

Holding periods by industry

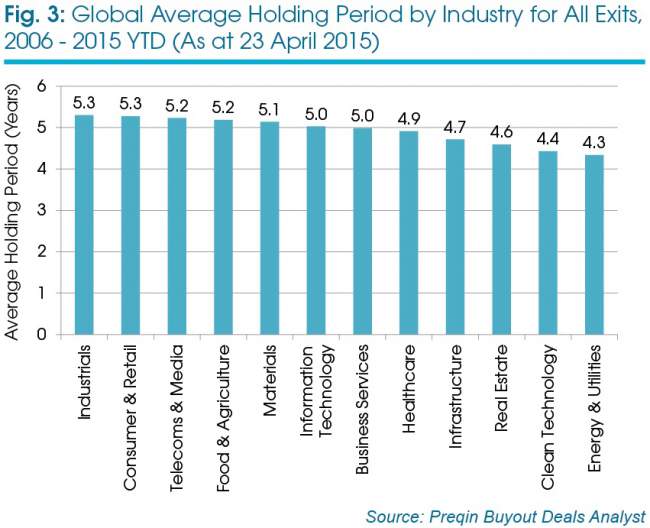

Fig 3 displays the average holding periods for the period 2006-2015 YTD, broken down by the portfolio company’s industry. It is apparent that portfolio companies in the industrials, and consumer & retail sectors have on average had the longest holding period of 5.3 years, while the companies operating within the energy & utilities industry have on average been held for one year less, with an average holding period of 4.3 years.

Size of deals

On average, deals across all size classes have seen holding periods lengthen over recent years, but large cap deals (USD1 billion or more) have seen the largest change since 2006, reporting a low of three years in 2008 and a high of seven years in 2014. A significant amount of large cap deals took place prior to 2008, with fund managers purchasing companies at peak prices during the buyout boom. Large cap deals accounted for 12% of the number and 79% of aggregate deal value in 2006, compared with 2009 when they accounted for only 3% of the number and 39% of aggregate deal value. The average holding period for mid cap deals (USD250-999 million) increased from just 3.2 years in 2006 to 6.4 years for portfolio companies fully exited in 2014; and for small cap deals (less than USD250 million) this increased from 3.5 years in 2008 to 5.8 years in 2014.

Exits

Although fund managers are largely holding onto portfolio companies for longer, the number and aggregate value of private equity-backed exits have been on an upward trend, with 2014 witnessing a record number and aggregate value of private equity-backed exits. Last year, 1,686 exits valued at a total of USD442 billion took place, indicating that GPs are still capitalising on suitable exit opportunities for their investments. This positive trend can somewhat be attributed to the increasing prominence of partial exits in recent years. Such exits accounted for a third (33%) of all exits in 2014 in terms of number of exits, compared with just 21% of all private equity-backed exits in 2006 and 19% in 2008.

This is an extract from the Preqin Private Equity Spotlight: May 2015. Read the full newsletter for free.