Returns offered by the private equity asset class are often a hot topic for discussion in the investment industry. With yields varying between fund types, sectors and managers, Jessica Duong (pictured) investigates the differences in performance of sector-specific buyout funds in this extract from Preqin Private Equity Spotlight – June 2015.

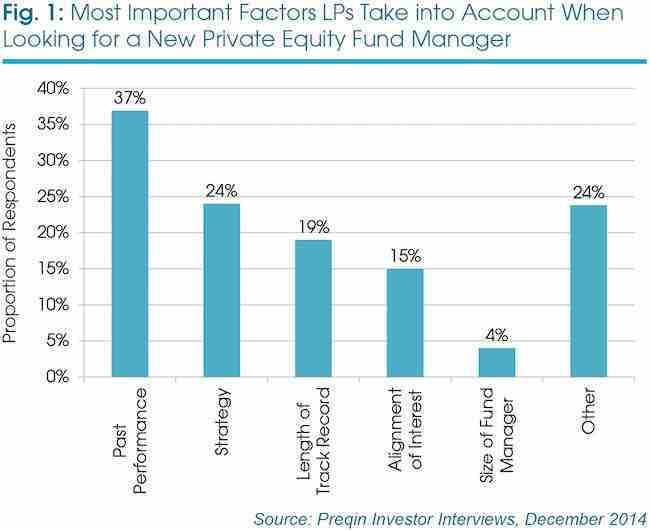

One of the main attractions of private equity for investors is the potential for outperformance over public equities over the longer term and the prospect of high yields. Offering insight into the sentiment of the LP community, Preqin’s latest global study of LPs revealed that 37 per cent of investors surveyed indicated that a GP’s past performance is the most important factor assessed when looking to partner with a new private equity fund manager (Fig 1).

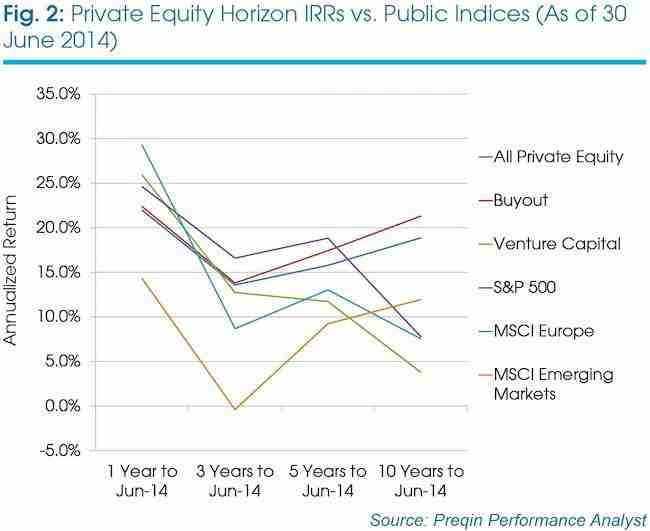

We can use Preqin’s Performance Analyst database to compare the horizon IRRs of public indices, private equity and, more specifically, buyout and venture capital, as shown in Fig 2. Over the 10-year period to June 2014, buyout and private equity as a whole outperform all listed indices shown by a significant margin, with buyout posting annualised returns of 21 per cent, compared to 7 per cent for the S&P 500.

Fundraising data shows that the majority of buyout funds through the years have been diversified in investment focus, both in terms of the number of funds raised and the aggregate capital secured. Yet for many investors, a manager’s ability to demonstrate deep expertise in a focused field is a key differentiator, with the belief that a deep knowledge of specific industries will lead to more well-informed investment decisions. Is there a difference between the performance of funds that are diversified and those that specifically target investments in one sector? This article will explore this question, using the latest data on buyout fund performance from Preqin’s Performance Analyst online service.

Top-quartile performers

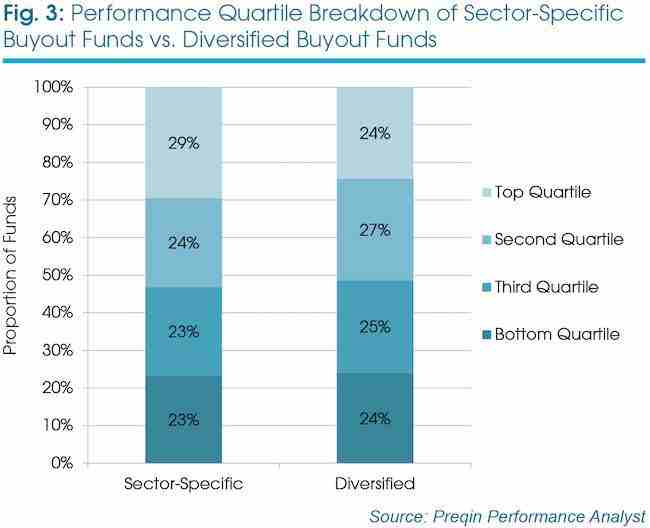

Using Preqin’s performance metrics for 1,690 buyout funds, with vintages ranging from 1982 to 2012, we can compare the performance of sector-specific and diversified funds (Fig 3). What instantly stands out is the greater proportion of sector-specific funds that rank as top-quartile performers: 29 per cent compared to 24 per cent of diversified buyout funds. While no guarantee of future performance, this analysis shows that those fund managers that exclusively target one industry have historically been more likely to achieve top-quartile returns.

Variable performance within sectors

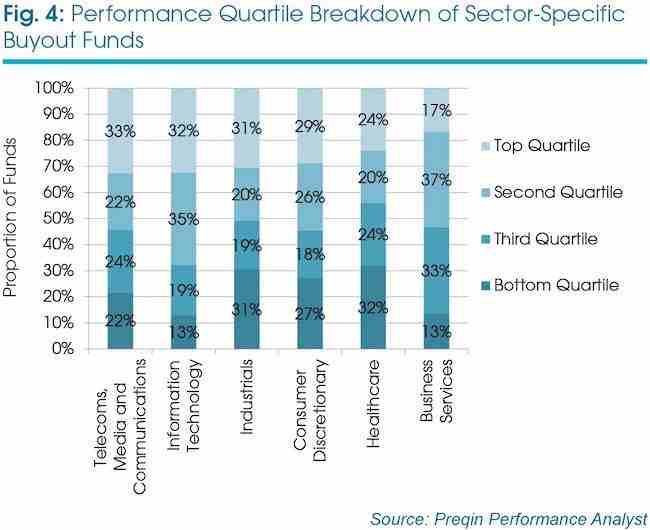

However, returns can also range quite significantly within individual industries. Fig 4 illustrates the mixed fortunes of sector-specific funds, with some industries attaining excellent track records as significant proportions of funds become top performers and/or see only a small minority of funds falling into the bottom quartile. The most remarkable of the industries shown, in terms of relative levels of success, are the telecoms, media and communications (TMC), and information technology (IT) sectors. A third of vehicles exclusively focused on the TMC sector, and a similar proportion (32 per cent) of solely IT-focused funds, qualify as top-quartile performers. Only 13 per cent of buyout funds focused solely on investing in the IT industry became bottom-quartile funds – a significantly smaller proportion than that of all other sectors shown in Fig 4, with the exception of buyout funds targeting business services.

The last decade has been an age of consumer-led technological change, with astronomic growth in the use of smartphones, tablets and mobile apps. Technological innovation in conjunction with economic and social trends across the world has driven this change, leading to a wealth of private equity investment opportunities. Rapid rates of infrastructure development, especially in emerging market regions, burgeoning middle-class populations and increased levels of disposable income are all factors that will have contributed to the continued flow of capital into the consumer market and heightened the appetite for advances in the TMC and IT sectors.

Conversely, almost a third (32 per cent) of buyout funds exclusively focused on the healthcare industry rank as bottom-quartile performers. The healthcare sector has traditionally been associated with innovation and significant growth, encompassing several sub-industries including pharmaceuticals, medical devices, hospitals, biotechnology and more. Investments in the industry often serve as defensive holdings in bear markets owing to the constant global demand for healthcare services, but Preqin’s data highlights the range in quartile rankings of healthcare-focused buyout funds and therefore the importance of fund selection for investors.

Median IRR comparisons

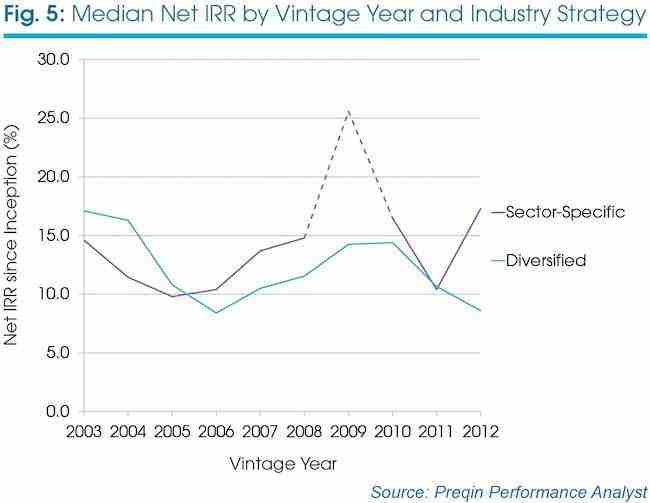

The median net IRR chart (Fig 5) shows the performance of buyout funds by vintage year and highlights the extent of the discrepancy between diversified and sector-specific vehicles over time. For earlier vintages, diversified funds showed a higher median net IRR; however, in 2005 the trend reversed. In certain years, the difference is quite significant: for vintage 2009, diversified funds had a median net IRR of 14.3 per cent compared with 25.6 per cent for sector-specific vehicles. However, it is worth noting that the spike in the chart for vintage 2009 sector-specific funds comprises data points for just four vehicles compared with 48 diversified funds for the same year. All four of these sector-specific funds achieved top-quartile returns when compared to buyout funds of the same vintage and geographic focus, with individual net IRRs ranging from 24.0 per cent to 41.5 per cent.

Preqin’s latest data for vintage 2012 funds shows that the difference between the two fund categories is considerable, and despite the gap narrowing in the years in between, sector-specific buyout funds appear to maintain the edge in terms of performance.

Outlook

As more performance data for more recent vintage funds becomes available, we will be able to see if this trend of sector-specific buyout funds generally outperforming their more diversified counterparts will continue. We also note that returns seen in the past offer no guarantee of future performance, placing more significance on the ability of the GP investment team and the importance of the LP’s choice of fund manager.

Meanwhile, statistics for the current buyout fundraising landscape reveal the continued bias for diversified funds. There are currently 277 funds seeking USD202 billion in aggregate capital; in terms of the split between sector-specific funds and those funds diversified in industry approach, only 39 per cent of buyout vehicles will invest exclusively in one industry, accounting for just over a quarter (26 per cent) of all capital sought. Figs. 6 and 7 list the top 10 buyout funds currently in market, highlighting the greater amounts targeted by diversified funds.

Another method of targeting specific industry sectors is via customised investment products; separate account vehicles have become increasingly prominent in recent years as the private equity asset class evolves and LP appetite for these structures increases. This year, an INR 60 million fund of funds focused on the agro-industry was established under India-based firm SIDBI, and New Jersey Division of Investment committed USD150 million in the NJ/HitecVision co-investment vehicle, which explores opportunities in the oil & gas industry. Hewlett Packard Ventures is another example of a vintage 2015 fund exclusively targeting one sector; the USD500 million separate account provides expansion-stage capital to technology start-ups.

Preqin’s Fund Searches and Mandates tool on the Investor Intelligence module shows that for the majority of LPs currently looking to make a commitment to new private equity vehicles, a diversified industry approach is on the agenda. Among the 18 per cent that are specifically looking at just one sector, there are a handful of industries that have attracted notable interest, namely the energy, technology and healthcare sectors.

This is an extract from Preqin Private Equity Spotlight – June 2015. To read the full newsletter, featuring league tables of the top 10 fund private equity fund managers by strategy, analysis of healthcare-focused fundraising and more, click here.