In this extract from the 2015 Preqin Investor Network Global Alternatives Report, we draw upon the latest data and investor interviews to explore the importance of alternative assets in an investor’s portfolio.

Private Equity

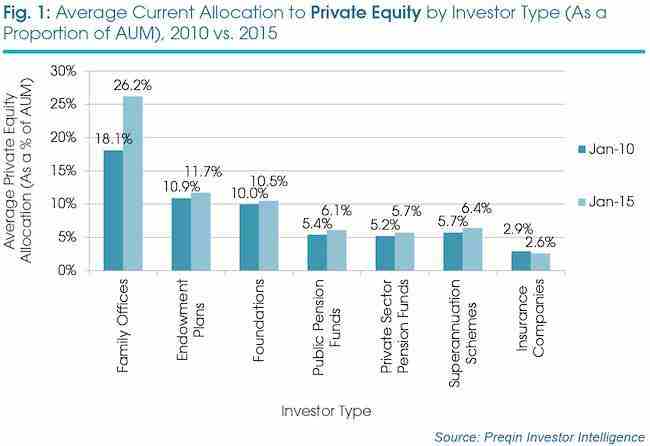

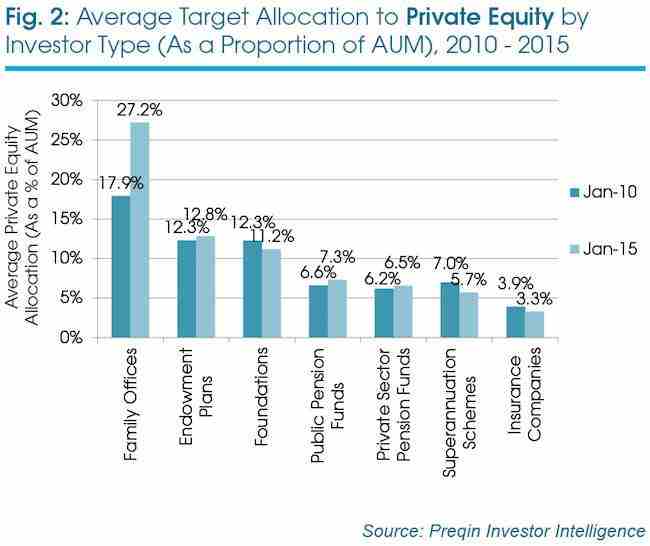

The limited partner universe has expanded and diversified in line with the growth of the private equity asset class. More investors are attracted to the asset class as a result of its consistent outperformance of public markets and the diversification it brings to investment portfolios. Examining average investor allocations to private equity over time by investor type provides insight into how different groups perceive the asset class, and what their investment intentions might be going forward.

Family offices maintain the highest current (26.2%) and target (27.2%) allocations as a percentage of their total assets when compared to other investor types (Fig 1 and Fig 2). This is more than double the average allocation of endowment plans, which hold the next largest mean current and target allocations at 11.7% and 12.8%, respectively. Regulations such as the Volcker Rule, Solvency II and Basel III do not inhibit family offices and they have fewer restrictions and more flexibility with their investment decisions than other investor types, making them attractive to GPs.

The only LP type to reduce both its current and target allocations to private equity over the past five years is insurance companies. This can be explained by the Solvency II directive, which specifies that Europe-based insurance companies must hold more liquid assets, and is expected to take effect in January 2016. However, for all investor types, average target allocations to private equity exceed average current allocations to the asset class. This is unsurprising as distributions continue to outweigh capital calls, prompting investors to look to invest additional capital in the future in order to maintain, and in some cases increase, their current exposure to the asset class.

Real Estate

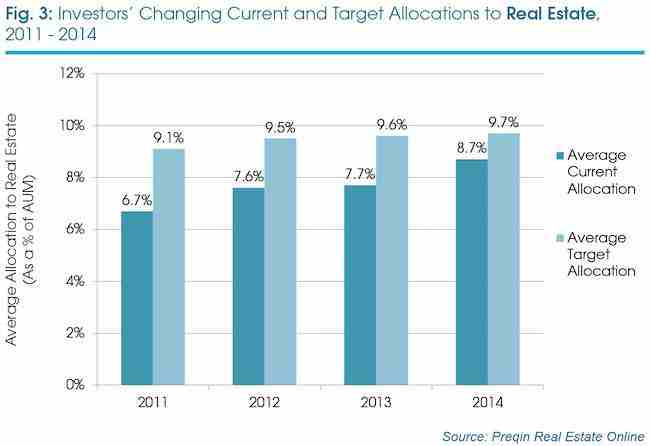

Due to the inherent lack of liquidity, investing in real estate is particularly suited to investors such as pension funds with long-term investment horizons. As a result, these investors are the most likely to have high allocations to the asset class. At 10.3%, superannuation schemes have the highest average target allocation of any investor type, followed closely by public pension funds at 10.2%, and private sector pension funds at 9.5%. Investors will look more towards investing capital in to the asset class in the medium to longer term in order to hit their allocation targets. Fig 3 shows that investors’ average current allocation has increased from 6.7% in 2011 to 8.7% in 2014, though currently all investor types are below their average target allocations to real estate. Over the same time period, investors’ average target allocation has increased from 9.1% to 9.7% as institutions have elected to up their target weightings to real estate.

Infrastructure

Due to the relative youth of the asset class, investors have typically allocated a smaller proportion of their assets under management (AUM) to infrastructure compared to the rest of their alternatives portfolio. However, the average current allocation to infrastructure has increased from 3.5% of AUM in 2011 to 4.3% in 2014, while the average target allocation to infrastructure has grown from 4.9% to 5.7% over this time period. Allocations to infrastructure are likely to continue to grow in coming years, with two-thirds of investors planning to increase their allocation to infrastructure over the longer term.

Private Debt

The growth of private debt as an asset class has also been a relatively recent occurrence and many investors have limited experience with the asset class, or are looking to make their first commitment. As a result, many investors are exploring how best to gain exposure to the asset class, with their preferences likely to evolve as they become more knowledgeable about the asset class, and how private debt fits into their overall portfolios.

As more investors become experienced within private debt, they will be more willing to deploy capital in the asset class. In February 2015, Preqin surveyed over 50 investors in the asset class, with no investors stating that they are currently above their target allocation to private debt. Half of investors were at their target, and the same proportion were under-allocated. Direct lending funds are currently the most favoured fund type among investors in private debt, with 62% stating the fund type is presenting the best opportunities in the current market. Half of respondents named special situations as also presenting strong opportunities. Interestingly, the two fund types that have traditionally dominated the private debt asset class, distressed debt and mezzanine, were stated by the lowest proportion of respondents.

Hedge Funds

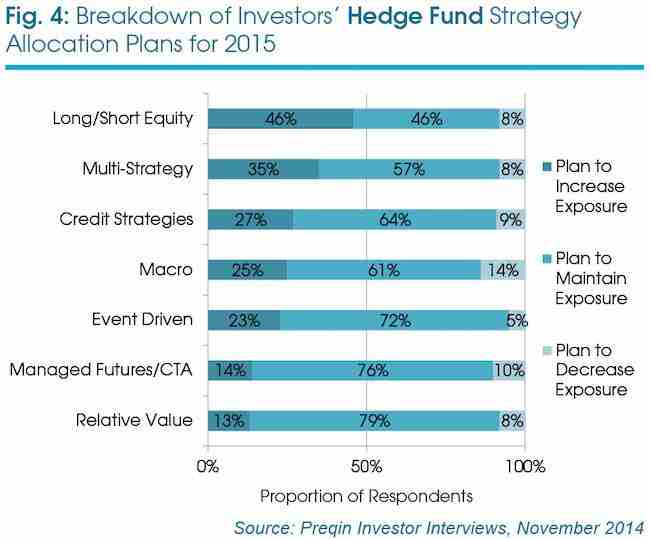

Investors allocate to hedge funds for their ability to produce consistent, risk-adjusted, absolute returns. In November 2014, Preqin asked over 135 investors about their specific plans for 2015 in relation to the strategy-weighting within their portfolios. Although 2014 was a disappointing year for hedge fund returns, across all strategies more investors were looking to increase their exposure rather than decrease exposure (Fig 4). Despite 36% of investors stating that the strategy had not met return expectations in 2014, nearly half of all investors surveyed with a current allocation to long/short equity intend to increase their exposure in the coming year. Thirty-five percent of investors also expect to increase exposure to multi-strategy funds, which was among the top performing strategies in 2014, as managers had the flexibility to shift their portfolios to exploit opportunities in the changing investment environment. Many of these investors may be looking to multi-strategy and long/short equity funds in order to reduce volatility within their traditional equity portfolios ahead of an uncertain 2015.

This is an extract from the 2015 Preqin Investor Network Global Alternatives Report. The report is currently free for accredited investors, qualified purchasers and alternative investment consultants on Preqin Investor Network (simply login or sign up to download), or available to purchase via our website for $175/£95/€115.