In an extract from the recently released Preqin Investor Outlook: Alternative Assets H2 2015, Preqin explores institutional investors’ plans for their infrastructure portfolios, including investment in alternative structures, and looks at the alignment of interests between investors and fund managers.

The infrastructure fund market is relatively smaller than those of other alternative asset classes; just over a third of institutional investors allocate part of their assets under management (AUM) to infrastructure, while over half invest in private equity, hedge funds and real estate. While there are some very experienced investors that have been active for some time, there are also many newer entrants that are relatively inexperienced. As these investors evolve and gain further expertise, they will explore new ways to gain exposure to infrastructure. As a result, it is vital that fund managers are aware of, and adjust to, changing investor attitudes in order to secure capital in a competitive fundraising environment.

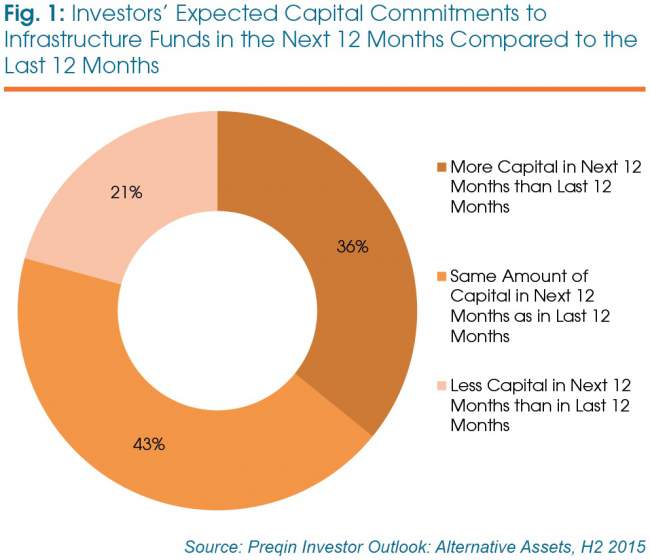

Investors’ infrastructure commitments in the next 12 months

As can be seen in Fig 1, 79 per cent of surveyed infrastructure investors expect to commit at least the same amount of capital as in the previous year. In comparison to results from December 2014, when 45 per cent of investors indicated that they expected to commit less capital to the asset class, these results are encouraging and demonstrate the continued importance of infrastructure in institutional investors’ portfolios.

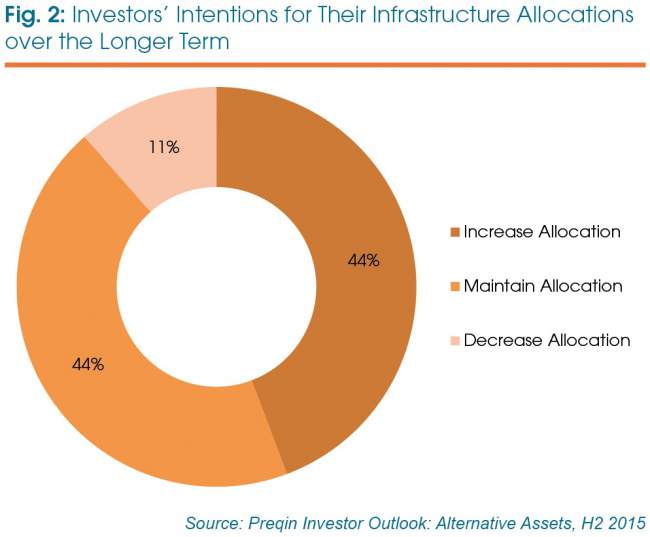

Investors’ infrastructure allocations over the longer term

Over the longer term, the prospects for the continued growth of the asset class are positive. The average current allocation to infrastructure across the entire infrastructure investor population has remained steady in 2014 and 2015 at 4.3 per cent of AUM. The average target allocation, however, has reached its highest level yet, at 6.3 per cent of total assets. Forty-four percent of survey respondents stated they will increase their allocation to infrastructure over the longer term, with a further 44 per cent maintaining their current level of exposure (Fig 2). Eleven percent of respondents plan to reduce their allocation in the longer term, representing a notable shift in attitude from the results at the end of 2014, when no investors intended to reduce their allocation.

Capital outlay and investment plans

Preqin’s Infrastructure Online service tracks the activity and plans for future investment of over 2,500 active investors in the infrastructure asset class. Over half (51 per cent) of investors with plans to make further investment in the next year will invest more than USD100 million in infrastructure opportunities, with 20 per cent of investors planning to invest over USD500 million.

With some investors planning to put considerable amounts of capital to work over the next year, it is positive that 48 per cent plan to invest in more than three new infrastructure vehicles, with 12 per cent planning to make at least five investments in the coming year.

The benefits of geographic diversification have led nearly half (48 per cent) of investors with plans to place additional capital in the asset class to target global opportunities. European and North American infrastructure assets are targeted by 41 per cent and 32 per cent of investors respectively. Despite the inception of the Asian Infrastructure Investment Bank by China and further plans for infrastructure funding from the Japan-led Asia Development Bank, Asian infrastructure assets are targeted by only 13 per cent of investors planning new investments.

Route to market

While appetite for listed infrastructure vehicles has remained low since 2013, interest in direct investment and unlisted funds has fluctuated over time. At the beginning of H2 2015, unlisted vehicles are targeted by the largest proportion of investors planning further capital outlay; three-quarters of investors choose this route to market, representing an increase from the 65 per cent at the end of 2014. Correspondingly, the proportion of investors targeting direct investment has fallen from 56 per cent in December 2014 to 46 per cent in June 2015.

Looking back further in time shows the growth of the asset class and the growing expertise of investors active in the market. In December 2012, 91 per cent of investors were targeting unlisted vehicles and 29 per cent were targeting infrastructure assets directly. As investors grow their AUM and build up distinct investment teams, it is expected more investors will target direct infrastructure investment.

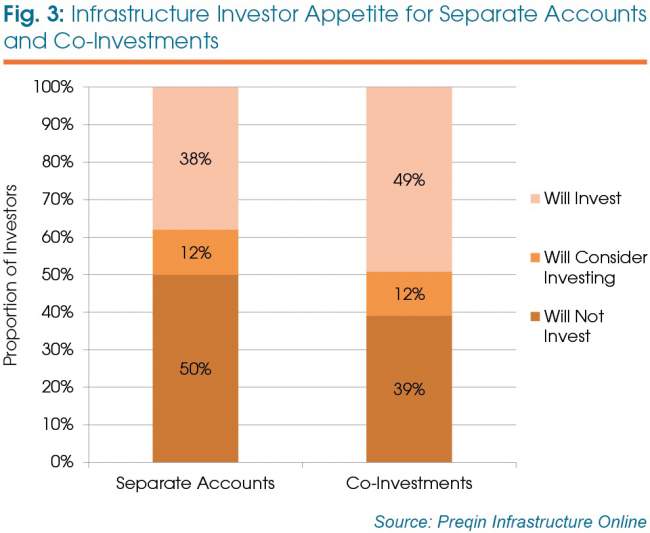

Alternative structures: Co-Investments and separate accounts

As institutional investors’ expertise in the infrastructure market develops, they start to look for alternative structures and routes to market as opposed to just investing in pooled infrastructure funds. The benefits include greater control over the direction of their capital, more access to attractive assets and a greater ability to negotiate fees and other fund terms. Fig 3 shows that 38 per cent of investors will seek to invest in separate accounts and 49 per cent will target co-investment opportunities alongside fund managers.

However, due to the high barriers for entry, these structures are typically only suitable for larger institutions. Often, this form of investment requires large capital commitments and substantial human resource to carry out the due diligence and portfolio monitoring that accompanies this type of investment. As AUM increases, investors are more likely to target both types of alternative structure; 57 per cent of investors with AUM of USD10 billion or more will invest in separate accounts, while 73 per cent of the same pool of investors will invest in co-investment opportunities. Comparatively, only 9 per cent and 36 per cent of smaller institutions (those with less than USD1 billion in AUM) will target separate accounts and co-investment opportunities respectively.

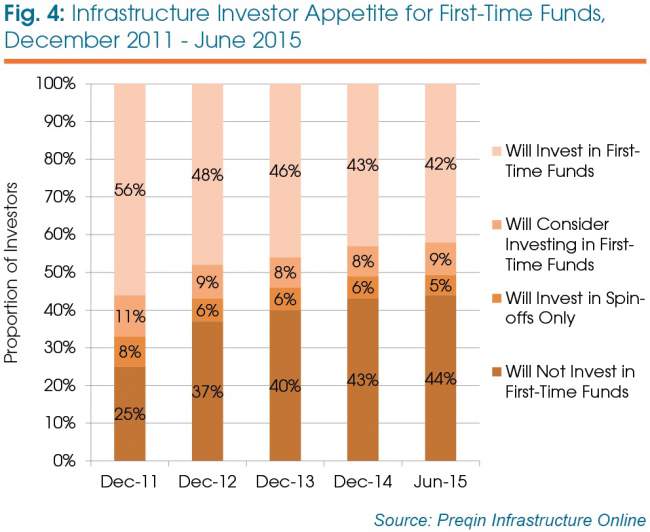

First-time funds

Investor appetite for first-time funds has continued to decline since 2011. As it stands, 42 per cent of investors will invest in first-time infrastructure funds, a slight reduction on 43 per cent in December 2014 and 56 per cent in December 2011 (Fig 4). Many institutional investors are increasingly keen to invest with managers that have a proven track record, and with 50 per cent of funds in market being raised by managers that have raised two or more infrastructure funds previously, investors are less likely to target first-time fund managers with capital likely to become further concentrated among the leading managers with established track records.

Fees and alignment of interests

A substantial 86 per cent of surveyed investors feel that investor and fund manager interests are properly aligned, or do not have a strong opinion either way, compared to 51 per cent of surveyed investors which stated the same in June 2013. This suggests that fund managers have largely listened to the concerns regarding fees and the growing requirement to adopt terms that better meet investors’ needs. Positively for the industry, 6 per cent of respondents strongly agreed that there is an alignment of interests between investors and fund managers, compared with no respondents suggesting this was the case in December 2014. Furthermore, just 15 per cent of respondents disagreed that investor and fund manager interests are properly aligned, compared with 28 per cent in December 2014.

The majority of respondents (63 per cent) have not seen a change in fund terms and conditions over the last year. However, more surveyed investors have seen changes to fund terms in favour of the investor (27 per cent) than have seen changes in favour of the fund manager (11 per cent). With fund terms and conditions being such an important factor for investors, it is not surprising that many investors surveyed stated that they have previously decided against investing in a particular infrastructure fund opportunity due to the proposed terms and conditions. In fact, 84 per cent of respondents claim they occasionally or frequently decide not to invest in a particular opportunity due to the fund terms and conditions, indicating that although the alignment of interests between investors and fund managers has clearly improved, work still needs to be done in some cases.

The fundraising environment is driven by the relationship between fund managers and investors. Key issues of fund terms and conditions and the alignment of interests between the two parties are central to creating a positive relationship and driving further capital commitments from the investor. Generally speaking, fund terms and conditions have become more favourable for investors over the last few years, and according to Preqin’s latest investor survey, a growing number of institutional investors are confident that fund manager and investor interests are firmly aligned, although fund terms do present a sticking point in some negotiations between investors and fund managers.

Outlook

With the majority of investors operating below their strategic target to infrastructure and expectations of further growth in allocations in both the short and long term, the outlook for the asset class appears positive. A multitude of economic, social and geopolitical factors will ensure further investment in infrastructure assets over the longer term, although in the short to mid-term, pricing concerns have affected infrastructure fundraising and made investors more cautious over where they commit further capital. New investor commitments are likely to become further concentrated among a smaller selection of experienced managers with a proven track record. However, growing investor sophistication and size have led to continued growth in alternative structures to pooled funds.

This article is drawn from Preqin Infrastructure Spotlight: September 2015. This edition of the free newsletter also features an examination of Japan’s infrastructure investor universe and more.