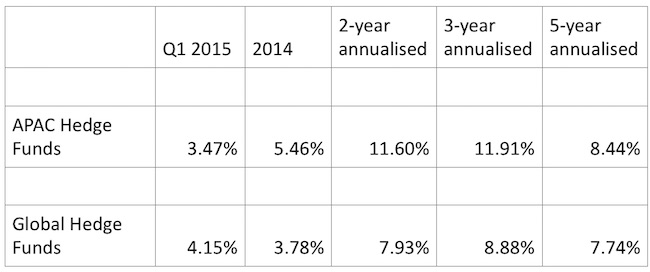

From a performance perspective, Asia Pacific-focused hedge funds have really stood out from their global peers, not just over the last 12 months but over a two- three- and five-year period. For anyone who still needs reassuring that APAC hedge funds can deliver value, simply consider the following numbers, as detailed by Preqin in its March 2015 Hedge Fund Spotlight report.

Much of this performance is being driven by exposure to equity markets in what remain the key economic powerhouses of the region; namely India and China. Managers who are embedded in the region and well placed to understand the machinations of its markets are reaping the benefits of smart stock picking and is a sign that the talent pool is deepening in maturity and expertise.

As Preqin points out, the best performing fund in 2014 was the Alchemy India Long-Term Fund, managed by Singapore-based Alchemy Investment Management. The fund returned an eye-popping 60.60 per cent net return and boasts a 12-month trailing Sharpe ratio of 2.87.

Other strong performers last year include the Merchant Commodity Fund, managed by RCMA Asset Management, which returned 59.29 per cent, and the Redart Focus Fund, a value-oriented long/short equity fund managed by Redart Capital, returning 57.45 per cent.

These are strong numbers and are sure to catch the attention of not just regional institutional investors, but global investors, as the search for octane-fuelled alpha generators remains a critical mission for their portfolio allocation strategy.

What makes Asia Pacific particularly appealing, however, is not just strong annual performance among a select number of managers, but an indication that performance across the board is now being achieved with less volatility and more rigorous risk management. If one looks at the three-year rolling Sharpe ratio for Asia-based hedge funds since 2012, up until April ’14 they by and large lagged global hedge funds (All hedge funds in Preqin’s classification), with an approximate Sharpe ratio of 0.70. Since then, however, the Sharpe ratio has climbed significantly and exceeded that of global hedge funds, climbing to 2.0 by October ’14.

What is perhaps even more telling is that the rolling Sharpe ratio of Asia-based funds vastly outperforms that of hedge funds with a focus on Asia but which are located outside the region: just 0.70 (approximately) compared to 2.0 (through the end of 2014). If anyone wanted evidence that local managers with local insights are better placed than their global counterparts when it comes to trading Asian markets, this is it.

Indeed, consider the following performance figures. Asia-based hedge funds returned 10.17 per cent in 2014. By comparison, Asia-focused hedge funds located outside the region returned just 3.70 per cent. For 2013, that performance dispersion is even greater: 14.04 per cent compared to 5.96 per cent.

The reason for the stronger performance in Sharpe ratio, which indicates the effectiveness of a manager to deliver risk-adjusted returns, can be explained by a reduction in the rolling volatility. Since February 2012, this has fallen substantially from over 9 per cent to just 2.76 per cent according to Preqin. That makes Asian hedge funds the least volatile compared to all other global categories.

For many years, volatility combined with ineffectual hedging strategies has turned investors off Asian hedge funds. According to the CFA Institute (citing GFIA, a Singapore-based consultancy firm), some 67 per cent of Asian hedge fund strategies in 2013 were long/short equities: for reference, Preqin has that figure at 62 per cent.

In 2008, when the global financial crisis struck, large numbers of Asian hedge funds were eviscerated. The reason being that they were too long-biased, chasing the markets but ill prepared to deal with a market downturn.

That now seems to be changing if these lower volatility numbers are anything to go by.

Back in 2013, Asia Pacific’s hedge fund industry was composed of approximately 760 funds running USD138 billion in assets under management. According to Preqin, that AUM figure now stands at USD145 billion, with some 2,213 hedge funds operating out of the region. Between 2013 and 2014, the industry attracted USD33 billion of net new assets, representing a 29 per cent growth.

For the last five years, I have long wondered why the region has failed to take the next step in terms of AUM growth. When would it recover back to the USD200 billion peak of 2007? Maybe last year’s figures are a sign that things are firmly back on track.

However, one good year does not a great manager make. In order for the industry to resonate with institutional investors, especially those located in the region, we need to see continued evidence of strong risk-adjusted returns. Increasingly, investors are willing to sacrifice a bit of upside for superior risk management. They don’t want to see double-digit drawdowns. They don’t have the stomach for that.

So the remainder of 2015 will be interesting for Asia-based managers. Can they rise to the challenge and show that their hedge fund strategies stack up just as well as global blue-chip names? Certainly, long/short equity managers are best placed to shine. According to Preqin, 41 per cent of 2015 mandates among Asia Pacific institutional investors are in long/short equities, followed by 27 per cent with a preference for event-driven strategies.

But whilst 82 per cent of investors in the region look set to keep faith with the asset class, top of their mind is the risk profile of the manager when doing their evaluations. Sixty-nine per cent cited this as the most important factor, closely followed by returns (54 per cent) and liquidity profile (54 per cent).

Something that should encourage start-ups and emerging managers is that only 46 per cent of investors cited an established track record as a key factor. Provided managers are running institutional-quality funds, with a COO and a robust operational and risk infrastructure in place, they have a chance to attract institutional dollars. What they can’t afford to do is get carried away simply riding the upside in Asian equity markets. Due care and attention is required to actively short the book or use an effective FX/options overlay (not just an Index-level hedge), else they won’t be taken seriously.

I personally believe that today’s managers have learnt the lessons of 2008 and that Asia Pacific’s hedge fund industry is on the cusp of something very exciting. There is tremendous talent coming out of India and China. Look at India’s hedge fund performance. According to the HFRI Emerging Markets: India Index, it has generated 36.95 per cent over the last 12 months.

The challenge Asian investors have is finding the best talent to invest with.